Blue-chip success hits holdings in Growth Portfolio

11th July 2014 08:50

One of the most notable features of the last quarter in the UK was the sell-off in medium and smaller company growth stocks. Investors started buying shares in larger companies instead.

This switch had a negative impact on the portfolio due to its large holding in , which has a bias to smaller- and medium-sized companies.

Commenting on the market's change in direction, Mick Gilligan, head of research at Killik & Co and the manager of our hypothetical £100,000 growth portfolio, says: "It is hard to know what triggered the sell-off. Technology stocks had been hit previously, but some had got rather frothy.

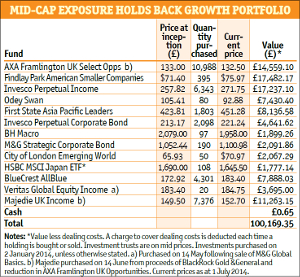

_0.jpg) QE concerns

QE concerns

"It may have been the result of hedge fund managers reducing their positions or the concern about the impact of tapering (of quantitative easing [QE]) on growth, or a combination of these factors. But consequently it was one of those rare quarters when the FTSE 100 index (of blue-chip stocks) performed strongly."

Gilligan had already started to reduce the portfolio's exposure to medium-sized growth companies during the quarter. In mid-May he told us of his decision to sell and invest the proceeds in instead.

The manager of the M&G fund had changed recently. However, Gilligan says that his main rationale for moving out of the fund was to increase his exposure to value in the larger company universe, where he thinks there are greater opportunities.

Veritas Global Equity Income is managed by Andy Headley and Charles Richardson. The group's investment philosophy is based on protecting and growing the real value of investors' capital. Headley and Richardson analyse all potential investments on an absolute basis, rather than relative to any benchmark or index.

Towards the end of June, Gilligan made two further switches. He sold his entire holding in and reduced the amount invested in Axa Framlington UK Select Opportunities by £10,000. The proceeds were reinvested into .

He says: "My reason for making these switches is to increase the portfolio's exposure to value-oriented stocks, while reducing its exposure to mid-cap growth, and to exit the gold miners on their recent strength. The gold-mining index has failed to exceed the recent high established in late March and looks technically weak in the short term.

Sterling strength

Even after this switch, Axa Framlington UK Select Opportunities remains the second-largest holding in the portfolio.

The portfolio's progress was also held back by the strength of sterling. , which is now the portfolio's largest holding, appreciated by 4.9% in dollar terms, but only rose 1.7% in sterling.

One of the reasons for the "incredible" strength of sterling, says Gilligan, is that the UK is the fastest-growing developed economy, it's attractive to overseas investors and is likely to be first place where interest rates rise.

was another holding which suffered from the conversion back to sterling. A rise of 8.4% in dollar terms declined to 5.1% in sterling terms.

Nevertheless, it was one of the portfolio's top-performing holdings during the quarter, along with the and , which all returned 5.1%.

Gilligan admits that it is difficult to know the exact reason for the success of BlueCrest AllBlue, a fund of hedge funds, other than that some of its strategies are obviously doing well.

In the case of , a long/short fund, Gilligan does know what went wrong. It was the portfolio's back marker in the quarter, with a fall of 7.6%. He says: "The fund was long of medium-sized companies which fell, and short of other stocks which went up in value and therefore had a negative effect on the fund."

Editor's Picks