GKN set to close the value gap

29th July 2014 11:51

A strong pound has been a significant headwind for and the City has shunned the automotive and aerospace engineer in recent months. But half-year results have proved them wrong. A 4% increase in underlying earnings per share easily beat consensus forecasts and the outlook statement suggests reasons for optimism.

Indeed, the share price, which recently hit a nine-month low, surged by over 6% on these six-month numbers. Yes, a £247 million currency hit trimmed sales by 1% to £3.8 billion, but organic revenue was up 6% as was underlying pre-tax profit, which strips out a big loss on forward foreign currency contracts last year, at £296 million. Adjusted earnings per share was 14.4p.

GKN's automotive businesses did especially well. Its core Driveline division continued to outpace 4% growth in global car production by some way. Organic sales grew by 11% to £1.76 billion and an increase in trading margin to 8%, which was also up slightly quarter-on-quarter, swelled trading profit by over a third to £142 million.

Powder Metallurgy, meanwhile - the other auto unit - ramped up sales by 6% and profit by a fifth, which helped offset a 9% decline at the land systems business where weak agricultural market knocked sales by 9% and profit by a quarter.

Over at the aerospace division, organic revenue grew by 3% to £1.1 billion and profit rose by 6% to £121 million - high demand for Boeing 787 and higher margin spares offset a dip on various military programmes.

Looking ahead, management reckons the planes division should continue to generate organic sales growth and automotive will keep beating the underlying market. Land will remain weak, but it's GKN's smallest division and the company is well-diversified enough to cope with that.

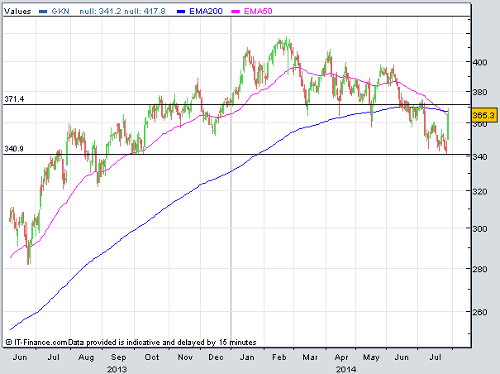

GKN shares have underperformed both the engineering sector and wider market this year. But after testing technical support at 341p, have bounced smartly. Yet, even now they trade on a forward price/earnings ratio of just 13 for the full-year, dropping to 11 for 2015. That's a 26% discount to the sector and looks incredibly harsh. Keep up this performance and there's every chance that gap will close in the months ahead.

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Editor's Picks