Mobile deal would be massive boost for BT

26th November 2014 14:12

by Lee Wild from interactive investor

Share on

Two days after admitted it was in talks to buy Telefónica's UK mobile operator O2, EE has confirmed it, too, is chewing the fat with the UK phone giant over a possible sale. In truth, this was the worst kept secret in the City, but confirmation means that with two happy sellers in the game, BT clearly has the edge at the negotiating table.

"Deutsche Telekom AG and Orange SA are in exploratory discussions with BT, although it is too early to state whether any transaction may occur," said the pair of EE, their mobile joint venture in the UK.

Spanish rag, El Confidencial, broke the news on Monday, suggesting Telefónica would sell O2 to BT and take a 20% stake in the company. It could take about £8 billion to return O2 back to BT, the company which hived it off in 2002 as mmO2 that was then bought by the Spanish for £18 billion three years later.

The telecoms team at Barclays are bullish on prospects if the O2 deal happens:

We already see BT as well positioned organically to add value in mobile, with potential for further upside through opportunistic inorganic acquisitions, given UK mobile operators currently struggle with low margins and competition remains intense.

Similar tie-ups in Europe - the Zon/Sonaecom merger into NOS, Numericable/SFR deal and Vodafone/ONO - have delivered big cost savings, and Barclays sees "clear potential for revenue synergies plus savings from churn reduction, retail distribution and network simplification".

Barclays reckons winning O2 could realistically drive total mobile revenues of between £1-2 billion for BT, implying a market share of 5-10%. It could significantly boost earnings, too - by 18% in 2017 and 17% the following year.

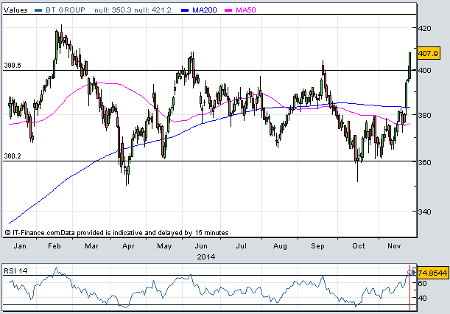

The shares have made another break above the 13-month trading range, and it will be interesting to see if they can make this move stick. They do look temporarily overbought, according to the relative strength index, yet a forward P/E ratio of 13 is a discount to the sector, and underlying earnings per share are tipped to generate a compound annual growth rate of over 7% out to 2017. The dividend should grow almost twice as fast.