Legal & General profit falls short

4th March 2015 10:48

by Lee Wild from interactive investor

Share on

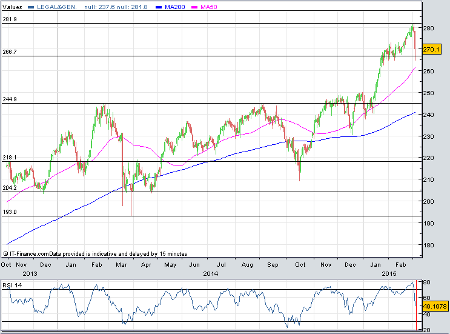

High-yielding insurer has been in an upward trend for the past six years in which time the share price has surged more than tenfold. The rally has been underpinned by the economic recovery, of course, with investment markets improving and the outlook largely positive. That's allowed L&G to ramp up returns to shareholders by gradually reducing dividend cover, and explains why the company is a favourite with income seekers. Full-year results reveal why the appeal is unlikely to fade any time soon.

Operating profit jumped by 10% to more than £1.27 billion, although that was a little below consensus estimates and is why L&G shares were down as much as 4% mid-morning. L&G Retirement did well, up 38% at £428 million, and L&G Capital made £203 million, 13% more than last year.

But the US business had a bad year, with profits down 39%. Management blamed mortality claims which were $46 million (£30 million) higher than its assumptions. "Mortality experience was generally unfavourable across the US life industry in 2014, especially in Q1 and Q4," warned the firm. L&G also included £31 million of restructuring costs in operating profit rather than take them below the line as they have done in the past.

Still, return on equity was up again, net cash grew to almost £1.1 billion and assets under management rose to more than £499 billion. European embedded value (EEV) shareholders' equity grew to almost £11 billion, equivalent to 185p per share, up from 162p the year before.

And the dividend rises rapidly, too. "Over the last five years we have increased dividend per share from 3.84p to 11.25p - a nearly threefold increase. In 2014 we produced another year of double digit growth across our key financial metrics enabling us to reward shareholders with a 21% rise in the dividend," points out chief executive Nigel Wilson.

Net cash dividend cover, down at 1.65 times, eases closer to the company's target of 1.5 times and from 1.82 times in 2013.

"Despite Legal & General's results today coming in slightly below forecast, they still highlight the expanding gulf between the insurance / fund management industry and the investment banks," says Rebecca O'Keeffe, head of investment at Interactive Investor.

"With assets rising, dividends up again and the return on equity reaching 16.9%, L&G's results are in stark comparison to Barclays' yesterday where their investment banking arm delivered a return on equity of just 2.7%. Increased regulation alongside the erosion of risk appetite has decimated the investment banking industry and investors may need to expand their horizons when looking for reasonable returns from financial companies.”

Clearly, a change to the pension laws allowing retirees to "cash-out" their pensions will hit sales of individual annuities. L&G thinks such sales will halve in 2015. It is chasing bulk sales to big companies in an effort to limit the damage, although margins are expected to come under pressure.

Panmure Gordon is confident though. "Despite the rally we believe that the share price has further to go and maintain our Buy recommendation and 305p/share target price. Return on equity has increased to 16.9%. Based on our 305p target price the shares would be trading on undemanding 2015/16F IFRS PE multiples of 16.1x and 14.9x whilst delivering an attractive dividend yield of 4.3% and 4.7% respectively."

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.