Trinity Mirror shares are "very cheap"

3rd August 2015 14:50

by Lee Wild from interactive investor

Share on

had cleared away much of the bad news in a gloomy trading update five weeks ago after which the share price slid to its lowest since 2013. But there's been a partial recovery this past week, and the Daily Mirror publisher's better-than-expected half-year results have extended the rally to 16%. There is evidence, however, that they could be worth far more.

As warned in June, underlying revenue once discontinued business is stripped out fell by 8.7% to £27.6 million for the 26 weeks to 28 June. Publishing revenue was down 8.8% to £254.6 million and print fell a larger-than-expected 13.6% to £24.2 million.

However, publishing digital grew by 26.8% to £18.9 million and group adjusted pre-tax profit fell just 2.5% to £47 million thanks to Trinity's tight grip on costs - it's recently doubled its annual cost saving target to £20 million and has cut capital expenditure by another £5 million. Revenue trends in July were better than during May and June, too, and although revenue is still falling chief executive Simon Fox says full-year results should hit forecasts.

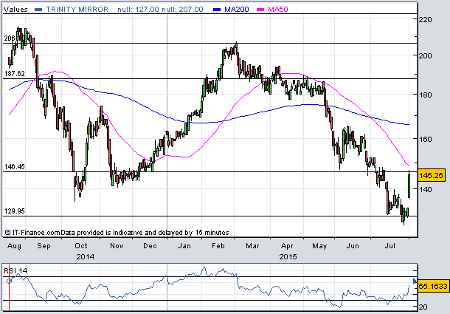

(click to enlarge)

Half-year results easily beat Numis Securities' own estimate for profit of £45.7 million, and the broker continues to pencil in profit before tax of £100 million for 2015, giving adjusted earnings per share (EPS) of 32p, down from £102.3 million and 32.8p respectively last year.

Trinity ended the period with net cash of £23.9 million versus £19.3 million of net debt at the end of 2014. That cash is worth over 9p a share and, despite costs both for the group pension and phone hacking scandal, can afford an interim dividend of 2p a share.

There's no further news on Trinity's appeal against "excessive and disproportionate" damages awarded to victims of phone hacking by its journalists. The extra £16 million set aside during the six months to cover the impact plus a £27.5 million gain on the sale of MeteoGroup in 2014 explains why Trinity's reported profit plunged from £50.5 million to £12.1 million.

"Trinity's share price is very cheap at current levels, it does not reflect the strength of current and expected cashflows in our view," writes Gareth Davies at Numis. "We reiterate our Buy recommendation and blended multiples based target of 298p."

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.