Four small-cap miners tipped for stardom

4th September 2015 13:44

by Lee Wild from interactive investor

Share on

Mining stocks have been in sharp decline since 2010, tracking the slump in global commodity prices. Mining companies have been slow to cut both capital programmes and unprofitable operations, resulting in significant oversupply of raw materials such as coal and iron ore. The heavyweights - among them , and - have seen share prices plunge by 60%, and the small and mid-cap plays are down 80% over the past five years.

"We contend that it will take at least a year for current surplus stockpiles of raw materials, intermediate products and finished goods to be absorbed by the market," warns Martin Potts, an analyst at broker finnCap. "However, in our view, prices of most mined commodities will have to start rising within the next two to three years."

"[We expect] most mined commodities to trade around their current levels for the rest of 2015 and 2016 before rising to at least the levels that justify further capital investment in the sector from 2017 onwards."

And Potts believes there are now bargains to be had for brave investors. Several mining stocks "offer good value with low inherent risks at current commodity prices," he says, all of which are either profitable and paying dividends, are just entering production or are fully funded to positive cashflow "and can confidently be bought today".

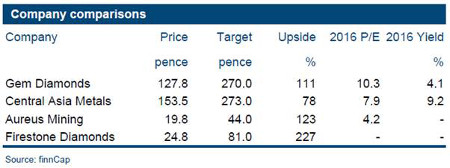

The four companies on Potts' buy list - covered in order of risk, from lowest to highest - all offer considerable upside to finnCap's target prices and retain "unusually low risk profiles relative to other small to mid-cap mining stocks".

(click to enlarge)

already makes lots of money selling unusually large and high-quality diamonds. Its Letšeng mine in Lesotho produces the most valuable diamonds of any diamond mine in the world, and demand from super-rich buyers has held up better than for mass market diamonds. Cash generated from Gem's mining portfolio is expected to be returned to shareholders by means of a dividend. The first was paid in June and Potts reckons this will grow from the present 4.1% yield as it is currently more than three times covered by earnings.

also makes big profits. It recovers copper from old waste dumps at the Kounrad copper mine in Kazakhstan, explains Potts, and even at present copper prices, the business has an operating margin of 65%. Highly experienced management have a track record of creating and returning value to shareholders, and the shares currently yield 8.6%.

Having now finished building its New Liberty gold mine in Liberia, is ramping up to full production. It's a high-grade resource for an open-pit mine, so margins will be high. "The market does not appear to recognise that first cashflow is imminent, as the stock is trading at just 4.2x 2016 earnings," says Potts. "We expect that the stock will re-rate once it declares commercial production in Q4 2015."

Lastly, and the higher-risk prospect, is . It's still more than a year from first production at the Liqhobong diamond mine in Lesotho - Q4 2016 is the current best guess - but Firestone is at least fully-funded through to positive cashflow. "This is one of the last really cheap entries into the diamond space apart from pure explorers," Potts says. "The Liqhobong project is also known to contain very large diamonds; these give the project considerable additional upside potential.

"Firestone is currently trading at less than 30% of our risked valuation, and consequently offers an exceptional investment opportunity on a two-year basis."

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.