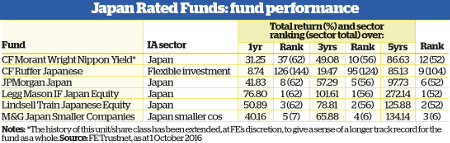

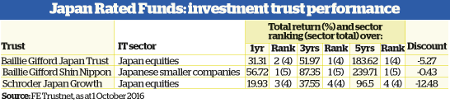

Are Japan's reforms a buying opportunity?

18th November 2016 12:24

by Marina Gerner from interactive investor

Share on

Low growth, low inflation and poor stockmarket returns in Japan mean the outlook for the country does not at first sight look promising. The strength of the yen and the Bank of Japan's underwhelming efforts to devalue the currency and stimulate the economy have not been successful thus far.

However, this year Japanese prime minister Shinzo Abe has strengthened his coalition's position in government, which should make it easier to introduce more decisive expansionist policies.

We consider the economic and political backdrop and their likely impact on the Japanese stockmarket, and ask what kind of funds are best placed to do well in the months ahead.

Abenomics making slow progress

Reiko Mito, manager of the , takes a positive view. She says the profitability of Japanese companies "is at a historic high, but the stockmarket, Topix, has been going nowhere".

She adds: "We are still making a slow recovery. There is sustainable GDP growth of around 0.5-1% in the Japanese economy." But she cautions that analysts have been too optimistic about the speed of economic change.

The economic policy of the past few years, known as Abenomics, is based on three "arrows". The first relates to monetary policy and aims to combat deflation through the money supply.

The second is about fiscal policy, principally increasing government spending to stimulate demand in the economy. The third refers to structural reforms to make the Japanese economy more productive.

Japan faces major problems, including how to overcome deflation and step up efforts to deal with the country's ageing and declining population, says Hideo Shiozumi, manager of the .

"We believe that with Abenomics, under the prime minister's strong leadership, Japan has a good chance of overcoming deflation and revitalising its economy." In the upper house elections, the ruling parties won a majority of the 121 contested seats, and voters showed confidence in Abe.

Abenomics pressed the accelerator for the corporate sector, but hit the brakes for householdsThe first arrow (monetary easing) of Abenomics significantly weakened the yen in 2013. This boosted corporate profits, but households did not benefit, as the weakened yen pushed the prices of many products higher, eroding standards of living.

The second arrow (fiscal policy) involved reducing corporate tax rates and raising taxes for consumers. Again, the corporate sector benefited, but households suffered.

Shiozumi says: "Abenomics pressed the accelerator for the corporate sector, but hit the brakes for households."

Sensible policies

Sarah Whitley, head of Japanese equities at Baillie Gifford and fund manager of the , believes the second arrow has probably been the least successful one.

"Abe hasn't worked effectively with the finance minister, who keeps tightening fiscal policy. This doesn't help overall GDP growth."

Whitley does not think Japan is going to experience rapid GDP growth, but she believes Abe's policies "to break Japan out of its deflationary mindset" are very sensible.

She says that despite the country's inability to sustain headline inflation recently, "at the core inflation level, which strips out fresh food and energy, there is inflation in Japan".

She adds: "What hasn't happened is any significant change to the deflationary mindset, despite the fact that land prices are rising nationwide. It seems to be a very difficult thing to change."

Whitley's hope for the next five years is that Abe's policies reshape that attitude. Currently, personal financial assets are 2.5 times nominal GDP, and a lot of that is in cash, under mattresses and in safes.

Companies with childcare services on site get tax credits to boost numbers of women in workShe says: "If the mindset were to change, the scope for improvement in equity markets would be enormous. [Similarly, at a corporate level] companies are thinking about paying out more dividends.

"They have masses of cash on their balance sheets, but they too are still in a deflationary mindset."

So what has worked well? Mito argues that structural reforms (the third arrow) in the childcare area are promising. The number of childcare places is to be increased by 500,000 over the next two years.

This is an important step in raising the labour participation rate of women. Companies that build childcare services on site receive tax credits.

Immigration and tourism

Whitley welcomes greater female participation in the workforce. She says: "If as a nation you don't want significant immigration, you need to use your existing population more effectively."

The foreign population in Japan is now at a record level, and the country is less inward looking. People realise that with its ageing demographic, Japan will need to find labour from elsewhere.

Mito commends Japan's move to make it easier for foreigners to get visas. She says: "It has been hard to convince voters, who are very anti-immigration.

The most spectacular success for the economy is the increase in inbound tourism"The current visa deregulation mainly applies to blue-collar workers, who mostly come from China, Vietnam and Malaysia. The government is gradually getting people used to having such people in the country."

Whitley says the most spectacular success for the economy is the increase in inbound tourism. The original aim was to have 20 million tourists visit by 2020, but that target was achieved by 2015. The aim now is for 40 million visitors by 2020.

"[The rise] has been achieved by providing more low-cost flights to Japan and making visas for visitors from Asia easier to obtain."

Another policy move Whitley deems hugely important is this year's introduction of a new tax and social security ID system called "my number". She thinks this will help tighten up on tax avoidance over the next five to 10 years.

Growth areas, disruptive companies

As bottom-up growth investors, Whitley and her team look for companies that operate in growth areas and disrupt existing business models. She has significant investments in internet-related companies.

One of her holdings is Softbank, which operates mobile networks in Japan and the US. It has a stake in Chinese e-retailer Alibaba and has just acquired UK chip manufacturer Arm Holdings.

Whitley's biggest overweight positions are in industrials, machinery and manufacturingWhitley's other holdings include Rakuten, Japan's largest e-commerce company, which has a fintech business, and Cyber Agent, one of the largest online ad agencies in Japan. She avoids the banking, chemical and steel industries.

Mito says her biggest overweight positions continue to be in industrials, machinery and manufacturing. One of her holdings is air conditioning manufacturer Diking, which has a very good market position in China.

She says: "Even during the slowdown in China it continued to grow, because it has strong distribution and good connections with small constructors."

Rich pickings for stockpickers

Mito also likes consumer staple companies such as Kao, which produces nappies, napkins, detergents and cosmetics. It has a very high market share in China, where people now favour higher-price-point nappies, she says.

Mito has a concentrated portfolio of 24 holdings in her fund, which she selects for the long term. Over the past eight years, she has only executed 17 trades. Every year her team makes one or two trades, and they hold companies for at least for five years.

She says the hype around Abenomics has died down, so it is no longer possible just to pick stocks that will benefit from the weakening of the yen. Now it is important that companies can manage their foreign exchange exposure.

Shiozumi's strategy is to invest in growth companies, particularly internet-related companies (including e-commerce firms), as well as medical, healthcare and other businesses set to profit from the country's demographic predicament.

Many central banks know how to deal with inflation, but few have dealt with deflationIn September, the Bank of Japan announced further quantitative and qualitative easing measures. It has kept interest rates at -0.1% and has decided it can pump as much money as it chooses to into the economy.

It will allow inflation to overshoot its previous 2% target. It aims to keep 10-year bond yields at zero.

Ed Smith, asset allocation strategist at Rathbones, is unconvinced that the bank's measures will succeed, but he maintains that stockpickers can still find rich pickings.

He says: "We lowered our exposure to Japan on the back of a disappointing macro picture that has soured earnings sentiment, but we remain overweight, as many companies continue to improve returns on equity, increase dividends and expand share buyback programmes, despite the macro. The bank's announcement seems unlikely to alter that backdrop."

As Whitley comments: "Many central banks know how to deal with inflation, but few have dealt with deflation. There isn't a road map for the Bank of Japan."

This article was originally published by our sister magazine Money Observer here

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.