Emerging markets are flying: Time to buy?

15th November 2017 09:08

by Cherry Reynard from interactive investor

Share on

After almost a decade of lacklustre returns for emerging market investors, all their Christmases have come at once.

Over the past 12 months Chinese policymakers have given economic growth a boost, Brazil has parked its political troubles, commodity prices have been stable or rising and economic reform across emerging markets has continued apace. The result has been double-digit growth for investors in emerging market funds.

This is in sharp contrast to sentiment a year ago, when there were fears China would collapse under the weight of its debt, Donald Trump was planning to repatriate manufacturing at the expense of emerging markets, and the strong dollar was expected to dent exports and increase debt.

Investors' views started to change as they began to realise Trump's bark might be worse than his bite and that political risk was not confined to emerging markets. With this in mind, the discounts afforded in emerging stockmarkets no longer seemed justified.

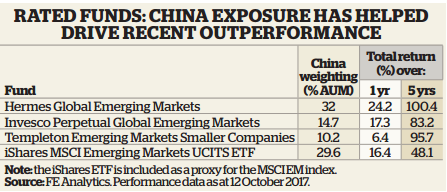

That said, investors have still had to be selective. Fund managers with higher weightings to China have done notably better this year than those with lower weightings. The MSCI China index is up 33% over one year to 29 September 2017, compared with 23% for the wider emerging market index. Exposure to emerging markets has been a key determinant of fund performance.

Technological triumph

The dominance of the technology sector has been part and parcel of this. Exciting, high-growth technology companies have outpaced the rest of the market, and a growing number are domiciled in China. The (top of the sector over the three years to 4 October 2017) has Samsung, and as its top three holdings. They are also the top three holdings for the (ninth in the list) and among the top four for the (third in the list).

For Gary Greenberg, manager of the Hermes fund, the reasons behind the dominance of the technology sector are clear: "The internet continues to take a greater share of the economy," he says. "Samsung owns the hardware side of that. Alibaba keeps delivering higher earnings than the market expects. They are not as expensive as the US FANGs (, , and ) and are showing better growth - of almost 50% in some cases."

This has been difficult for investors who remain nervous about China's debt problem or its corporate governance issues, and those who favour a more 'quality' approach.

The other notable phenomenon has been a reversal in the 'value versus growth' trend. Gavin Haynes, investment director at Whitechurch Securities, says that, as in other markets, value-focused funds have had a difficult time in recent years, but this trend has reversed with the cyclical recovery in emerging markets since 2015.

He adds: "Some of the 'higher-quality' stocks may have become over-owned and overvalued. They are good quality, but are the valuations justified?"

As a result of the reversal, a number of income-focused funds are at the bottom of the emerging market tables. and Newton Emerging Income have both seen reasonable growth over the past three years, of 30 and 26% respectively, but they have not kept pace with the wider sector. The Newton fund has just 6% in China, compared with 34% for the growth-oriented Baillie Gifford fund.

This remains a sector where active funds are firmly ahead. In the UK all companies sector, trackers generally sit around mid-table - the , for example, is 120th out of 248 funds in the sector.

The emerging markets sector, in contrast, contains only a handful of trackers, and they are all gathered towards the bottom third of the table.

The is the strongest performer, at 51st out of 89 funds. This is in spite of relatively high weightings to China (29%) and to some large technology names.

Structural growth

A number of funds haven't participated much in either the technology or the China trend, yet they still stand out as strong performers. The Jupiter Emerging Markets fund, run by Ross Teverson, has just 15% in Chinese equities and an eclectic mix of top-ten holdings that includes Brazilian educational group Kroton Educacional and Indonesia-based real estate developer Bumi Serpong Damai Tbk.

Teverson says: "A number of structural growth opportunities are only available in emerging or frontier markets. They have already played out in the West. These might include air travel and mortgage penetration." He believes such trends can often be sustained for decades.

The question for emerging market investors today is whether the growth rate of the past year can be sustained.

Teverson points out that valuations in emerging market equities are still below those in developed markets, and that emerging markets are in a completely different phase from developed markets in their economic cycle.

He adds: "Inflation and interest rates are coming down, and there is still room to cut rates. This should promote economic growth and expansion."

China aside, emerging markets have much lower debt. Most emerging market governments learned lessons in the wake of the Asian financial crisis, following a stable growth path since.

If there is another downturn in developed market economies, emerging market governments will have less dollar-denominated debt, more intra-regional trade and less vulnerability.

China remains the elephant in the room. Opinions are mixed as to the risk presented by Chinese debt. Some believe it is no worse than the debt burden faced by, say, the US, and that China's faster growth should erode its debt relatively quickly. But the IMF recently warned: "China's current credit trajectory is dangerous, with increasing risks of a disruptive adjustment."

However, Greenberg believes the biggest risks to emerging markets come from outside. He says: "The US market is very extended and could suffer a serious correction. We believe emerging markets would go down less, but it depends when it happens."

Fund Profile: Hermes Global Emerging Markets

Gary Greenberg, manager of the Hermes Global Emerging Markets fund, says there are trends in emerging markets that don't just replicate those in developed markets but improve on them. In many cases, they are bypassing a whole layer of development. Investors have been slow to recognise the opportunity, he says.

He points to initiatives such as WeChat, the messaging service owned by Tencent. This, he says, allows users to send money to their friends, do video conferencing and auto-translate.

"There is an explosion in interesting things to do on it," he adds. Internet penetration is higher in China than anywhere else in the world, and e-commerce is double that of the US: "Chinese consumers are very open to buying online." They are bypassing the development of the high street.

Holdings such as Tencent, Alibaba, Samsung and Taiwan Semiconductor - all of which are among Greenberg's top 10 holdings - have driven the performance of the fund in recent years. All are strong, emerging market businesses facing relatively little competition from their international peers.

However, this is not the whole story. Greenberg also likes 'old economy' companies that put technology to good use in their supply chains to promote efficiency.

He points to companies such as Bharat Forge, an Indian truckmaker with 45% of the North America market, and China-based Hikvision, which makes video surveillance equipment that applies artificial intelligence to camera images.

The fund is top-quartile over one and five years, and top of the whole sector over three years.

It launched in 2008 and now has $2.7 billion (£2 billion) under management.

Surprisingly, it has also fallen relatively little in periods of emerging market weakness.

This may in part be attributable to the environmental, social and governance considerations that Greenberg incorporates in his investment process, in common with other Hermes managers.

The fund is predominantly a stockpicking fund, although Greenberg does apply a macroeconomic overlay. He wants 'great companies' - loosely defined as those with great products, good market positions, solid balance sheets and a strong reputation.

At the moment, he is finding more of those in China than in, say, Brazil, where opportunities are more cyclical.

He believes hesitant investors have not yet missed the emerging markets boat. He says: "The growth is stronger and the stocks aren't expensive. Things are looking good."

This article is for information and discussion purposes only and does not form a recommendation to invest or otherwise. The value of an investment may fall. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

This article was originally published in our sister magazine Money Observer, which ceased publication in August 2020.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.